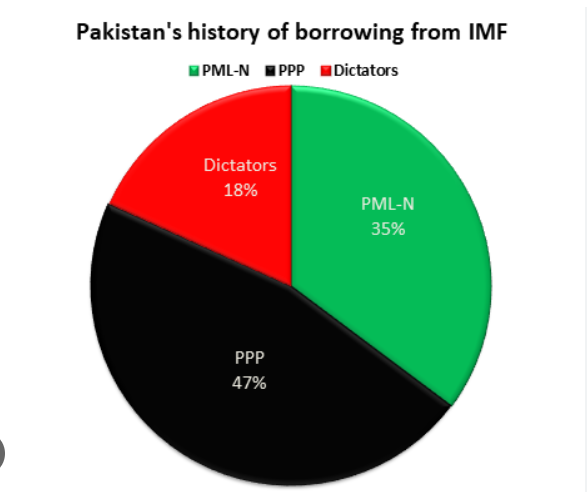

Pakistan: Ahead of February NA polls, IMF approves a $ 700 mn loan tranche

Virendra Pandit

New Delhi: Even as Pakistan’s economy is expected to grow at a meager 2 percent in the fiscal year 2024, the International Monetary Fund (IMF) tried to keep Islamabad’s nose up from drowning in bankruptcy by sanctioning another loan tranche of USD 700 million, ahead of the February 8 elections to National Assembly, the Lower House of Parliament.

The IMF on Thursday approved this bailout aid, under an existing USD 3 billion package, after completing its first review by the Executive Board of the Washington-based lender, the Dawn newspaper reported.

The cash-strapped South Asian nation won the final approval for the disbursement of this tranche from the global lender, providing a boost to the embattled economy.

Pakistan’s dollar bonds were among the biggest gainers in emerging markets for the day, with 2026 notes jumping 3.1 cents to about 70 cents on the dollar.

Islamabad’s performance under the program “has supported significant progress in stabilizing the economy,” Antoinette Sayeh, IMF’s Deputy Managing Director, said in a statement posted on the website.

“There are now tentative signs of activity picking up and external pressures easing.”

Pakistan’s economy might grow 2 percent in the fiscal year 2024 after contracting in the previous year, the IMF said. The nation’s dollar bonds delivered returns of over 90 percent last year as default risks eased following the global lender’s bailout, catapulting them into the top rankings in emerging markets.

The IMF funds are critical for Pakistan to secure financing from other creditors like Saudi Arabia and will give a boost to Islamabad’s caretaker government under Prime Minister Anwaar-ul-Haq Kaka ahead of elections.

Despite the aid, Pakistan remains under financial strain. The nine-month IMF program is set to end in March and Interim Finance Minister Shamshad Akhtar has already signaled the nation may need another loan from the IMF to support the economy. Pakistan has about USD 1 billion in dollar-denominated debt due in April 2024.

The IMF said Thursday that Pakistan needs a market-determined exchange rate to buffer external shocks, and a tight monetary stance to ensure that inflation returns to more moderate levels. It should also boost foreign reserves, the IMF said, with the latest data showing reserves stood at USD 8.2 billion in early January.

The Pakistani Rupee (PKR) has stabilized in recent months after sliding to a record low in early September. The currency traded at 281 PKR per US dollar on Thursday.

The IMF has now disbursed a total of about USD 1.9 billion under the program, it said. The approval came after the IMF Executive Board completed the first review of the USD 3 billion Stand-By Arrangement program approved in July 2023, and followed a staff-level agreement in November.

An IMF mission reviewed the country’s economic performance during the first three months of the fiscal year – from July to September 2023.

The completion of the review allowed for an immediate disbursement of USD 700 million in Special Drawing Rights (SDR), bringing the total disbursements under the Stand-By Arrangement (SBA) to USD 1.9 billion, Pakistan’s Finance Ministry said in a statement.

The initial tranche of USD 1.2 billion of the current IMF program was released in July 2023.

The other two tranches were subject to reviews, the first of which has been completed, while the other one will be in December, The News International newspaper reported.

In November 2023, an SBA was reached between the IMF staff and Pakistani officials regarding the first review under Islamabad’s SBA.

The global lender signed a nine-month USD 3 billion financing arrangement with Pakistan in June 2023 to provide the debt-struck country with a short-term loan.

Pakistan’s economy has been in a free fall mode for the last many years, bringing untold pressure on the poor masses in the form of unchecked inflation, making it almost impossible for a vast number of people to make ends meet.

Pakistan had been struggling to arrange enough foreign exchange to satisfy the IMF, which refused to provide the remaining USD 2.5 billion out of a USD 6.5 billion loan program signed in 2019 and expired on June 30 last year.