Roving Periscope: Now, Bangladesh leads the charge against China’s debt-traps

Virendra Pandit

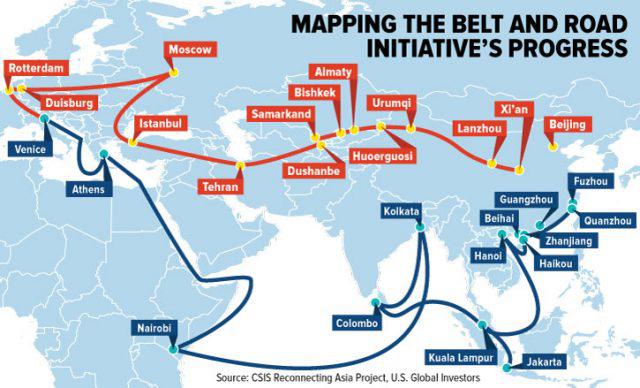

New Delhi: Learning a lesson from the fate of Chinese debt-trapped countries like Sri Lanka and Laos, Bangladesh has come forward to warn other nations against falling into this quagmire at a time Beijing itself feels its multinational, multibillion Belt and Road Initiative (BRI), a road to nowhere, may have become a white elephant it can neither get rid of nor kill.

According to the media reports, the BRI, which President Xi Jinping launched with much fanfare in 2013, is losing steam even within China, with few willing to put fresh Chinese investment in other countries which are still recovering from the post-Covid pandemic effects on their economies and cannot repay the loans.

This shows the Chinese economy’s reverses during the pandemic and its zero-Covid policy, which locked down several million people and industrial zones for weeks and months on the Chinese mainland.

With these headwinds, they say the BRI is being reviewed for its economic feasibility as several wary nations go against it and demand revision of terms and conditions. China’s secretive financial deals with recipient countries of the BRI projects are no longer confidential as these nations carefully scrutinize them.

Bangladesh has taken the lead in warning the world against the Chinese debt traps. Its Finance Minister AHM Mustafa Kamal has publicly blamed economically unviable Chinese BRI projects for exacerbating the economic crisis in Sri Lanka.

He has warned that developing countries must think twice about taking more loans through the BRI as global inflation and slowing growth add to the strains on indebted emerging markets, the media reported.

“Everyone is blaming China. China cannot disagree. It is their responsibility,” Kamal told the Financial Times. Bangladesh owes some six percent of its external debt to China and sought USD 4.5 billion worth of loans from the International Monetary Fund (IMF) in July to tide over its developing economic crisis.

Bangladesh and Nepal have told China they would accept grants, not any further loans. Having seen the economic collapse of Sri Lanka, which owes 10 per of its USD 51 billion external debt to Beijing, these nations have become extra cautious about the subtle Chinese moves.

In Sri Lanka, the white elephant of the Hambantota port is now virtually a Chinese colony. The way the British took Hong Kong on a 99-year lease that ended in 1997, Hambantota is also in the Chinese grip for 99 years since 2017 because of a debt-for-equity swap involving over USD 1 billion. The Rajapaksa International Airport there is also a non-starter.

The pathetic condition of China’s “all-weather friend” Pakistan is no different. It is reeling under a Chinese debt of nearly USD 53 billion, which Beijing is said to have spent so far on various projects under the overall USD 62 billion China-Pakistan Economic Corridor (CPAC). None of these projects is near completion.

The two countries had boasted of the CPEC as a major strategic initiative between “milk and honey” allies, but the Gwadar Port on the Makran coast is still incomplete, with Baloch separatists targeting the Pakistan Army and the Chinese workers.

The Gwadar port, once touted as an alternative to Dubai and Pakistan’s economic future, is quickly turning into a millstone around Islamabad’s neck. A bankrupt Pakistan is knocking on all the doors for aid. It is desperately seeking a multi-billion-dollar bailout from the IMF with depleting foreign exchange reserves, double-digit food, and fuel inflation—a double whammy of the Covid pandemic and Ukraine war—which is pushing Islamabad the Colombo way.

Likewise, the Chinese-funded USD 4.7 billion railway project in Kenya remained stalled. Interestingly, five years since its launch, it ended abruptly in an empty field, 200 miles from its destination in Uganda!

China’s debt traps in South East Asia are alike. Laos, which took huge loans from China for its large-scale infrastructure projects, is now at high risk of default.

International rating agency Moody’s downgraded Laos’ credit rating to Caa3 in mid -June, citing “a very high debt burden and insufficient coverage of external debt maturities by (foreign exchange) reserves.” Moody’s warned that Laos’ default risk will remain high, The Singapore Post reported.

In April, a World Bank report said Laos’ total public and publicly guaranteed debt reached an unprecedented 88 percent of the GDP in 2021. About half of this USD 14.5 billion debt is owed to China on loans to fund projects. These include the 418-km-long China-Laos Railway, a joint venture between the Beijing Railway group and two other Chinese government-owned companies with a 70 percent stake, and a Laotian state company with 30 percent.

The Kunming-Vientiane railway might link a future network to connect China with Thailand, Vietnam, Myanmar, Malaysia, and Singapore and give southern China more access to ports and export markets.

China has also invested nearly USD 44 billion in Indonesia, USD 41 billion in Singapore, USD 39 billion in Russia, USD 33 billion in Saudi Arabia, and USD 30 billion in Malaysia. Beijing has made massive investments in Cambodia because of which the ASEAN countries are mute spectators to the unilateral changes by China in the South China Sea and warmongering against Taiwan.