Roving Periscope: Turning off, Russian gas drags the euro down to under 99 cents

Virendra Pandit

New Delhi: The shadow of the inconclusive Russia-Ukraine war, which started on February 24 this year, and the subsequent West-led waves of sanctions against Moscow, have begun to impact Europe ahead of the biting winter ahead.

As Russia slowly turned the screws on the supply of natural gas to Europe, the Continent’s industries and people dreaded their future. The dependence of the European economy on Russian energy (petroleum and natural gas) is over 40 percent. This supply keeps European households warm in the winter and runs industries throughout the year. That shows why Europe was reluctant to clamp sanctions on its across-the-border Russia for its invasion of Ukraine but had to do so because of the remote US arm-twisting.

For the first time in two decades, the euro fell below 99 cents (INR: 79.83) as Russia, angry at the European Union’s support of Ukraine, tightened the screws on the Continent.

Around 341 million Europeans across 19 of the 27 members of the European Union (EU) use the euro as their common currency, making it the second most-used currency worldwide. The United Kingdom’s currency is better known by the word “pound,” while “sterling” is used in the financial markets.

Other members of the EU—Bulgaria, Croatia, Czech Republic, Denmark, Hungary, Poland, Romania, and Sweden—do not use the euro. Except for Sweden and Denmark, all of them are former members of the Soviet bloc. Russia is selectively plugging off gas supplies to woo them back into its fold.

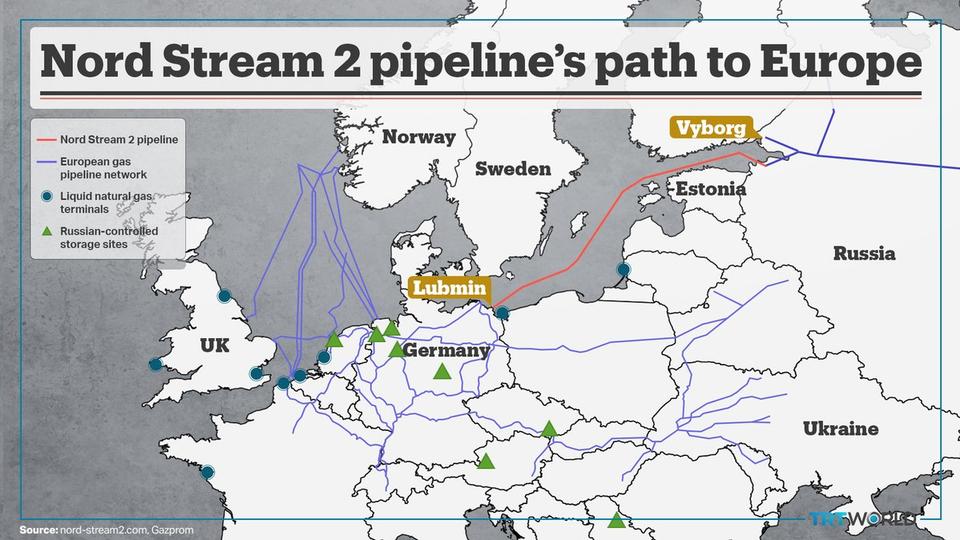

While the value of the euro fell, the sterling suffered grievously on Monday as Russia’s halt on gas supply down its main pipeline to Europe sparked concerns over energy prices and growth, the media reported.

The euro slipped to USD 0.9880 in Asia trade, the lowest level since 2002, while sterling hit a new 30-month low at USD 1.14445 and remained close to its pandemic trough.

Meanwhile, the US dollar index, which measures it against a basket of six currencies with the euro the most heavily weighted, hit a new two-decade high, surging to a top of 110.25.

Russia scrapped a Saturday deadline for natural gas flows down the Nord Stream pipeline to resume, citing an oil leak in a turbine. It coincided with the Group of Seven (G-7) finance ministers announcing a price cap on Russian oil.

The pound has also been weighed down by concerns over rising energy costs. British Foreign Minister Liz Truss, who may become the Prime Minister on Monday, said she would set out immediate action to tackle rising energy bills and increase energy supplies.

The Japanese yen, at 140.38 per US dollar, was also under pressure near a 24-year low. The risk-sensitive Australian dollar slid 0.41 percent and was near a seven-week low at USD 0.6780.

Now, Europe may resort to steep hikes in the interest rates this week. Markets have priced a near 80 percent chance of a 75 basis point (bp) hike in Europe and an almost 70 percent chance of a 50 bp hike in Australia.

In the United States, pricing for a 75 bp hike this month has pared back somewhat after a mixed jobs report on Friday last week that contained a few hints of a loosening labor market.

In Asia, the offshore Chinese yuan similarly fell to a fresh two-year low at 6.9543 per US dollar as worries linger over Covid-19 lockdown measures in the country.

China’s southern tech hub of Shenzhen said it would adopt tiered anti-virus restriction measures beginning on Monday, while Chengdu announced an extension of lockdown curbs as the country grapples with fresh outbreaks.