Virendra Pandit

New Delhi: Within a decade of its launch, India’s Unified Payments Interface (UPI) has almost pushed out the ‘traditional’ debit card from general use and the new, QR code-based system now powers 85 per cent of all payments, the media reported on Tuesday.

While the UPI dominates daily transactions, debit cards are rapidly fading from active payment behaviour; they still account for the bulk of cards but not used much.

Credit cards were introduced in India in 1961 when Kali Mody brought the Diners Club card to India. The first bank-issued credit card arrived in 1980 via the Central Bank of India (named the Centralcard, on the Visa network). The debit cards were introduced in 1998 following the rollout of India’s first ATMs by HSBC in Mumbai in 1987.

UPI

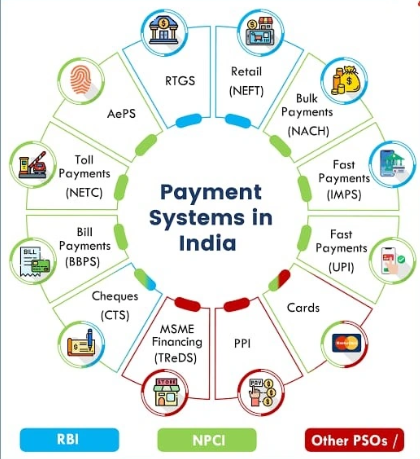

The UPI was officially launched on April 11, 2016. It was developed by the National Payments Corporation of India (NPCI) under the Reserve Bank of India (RBI) and has since revolutionized instant digital banking in the country.

India’s digital payments ecosystem is now overwhelmingly powered by tiny, everyday transactions, with UPI accounting for a massive 85.5 per cent of all payment volumes in the second half of 2025, according to the RBI’s latest Payments System Report.

That indicates Indians are now using UPI mainly for their day-to-day small-ticket requirements like paying for grocery purchases, utility bills, transport, etc.

The RBI report shows that digital payments now account for virtually all transactions in the country. During the first half of 2025, digital payments formed 99.8 per cent of total transaction volume, and 97.7 per cent of total transaction value.

UPI now accounts for nearly 49 per cent of global real-time payment transactions.

Digital transactions in India have increased 38 times in volume over 10 years, and more than tripled in value. In 2013, India recorded 222 crore digital transactions valued at Rs. 772 lakh crores; by 2024 that number surged to over 20,787 crore transactions worth Rs. 2,758 lakh crores.

UPI’s contribution to India’s digital payment volume rose from 34 per cent in 2019 to more than 85 per cent by 2025. The growth reflects how deeply UPI has penetrated everyday life.

The government recently said UPI processed over 24,162 crore annual transactions worth Rs. 314 lakh crores during 2025-26, making it one of the world’s largest real-time payment systems.

The debit card usage has stagnated, while QR-code and account-to-account payments surged.

However, UPI’s convenience, zero-cost transfers and merchant acceptance have increasingly reduced dependence on physical card payments.

India’s digital payment infrastructure is scaling rapidly. The report also points to rapid expansion in supporting infrastructure.

India now has crores of QR-code acceptance points, widespread merchant onboarding, and increasing rural payment penetration.

Credit Cards

While UPI dominates transaction count, debit card transaction volumes fell from 4.087 billion in calendar year 2021 to 1.336 billion in 2025, a 67 per cent drop over four years. Transaction value also declined from RS. 7.4 lakh crore to Rs. 4.5 lakh crore during the same period.

“While the decline in debit card transactions, both in volume and value, is potentially driven by the rise of digital wallets, UPI, and credit card adoption, debit cards remain more widely held than credit cards,” said the RBI report.

While debit cards are losing relevance in payments, credit cards continue to grow as a premium spending product. Credit card transactions more than doubled from 2.16 billion in 2021 to 5.7 billion in 2025, while transaction value surged from Rs. 8.9 lakh crore to Rs. 23.2 lakh crore, growing at an annual rate of around 27 per cent, per cent the report noted.

Private sector banks continue to dominate in the credit card space, focusing on digital and co-branded offerings for customers, as their market share increased from 67.7 per cent (4.8 crore outstanding cards) in December 2021 to 71.1 per cent (8.2 crore outstanding cards) in December 2025.

The share of Public Sector Banks (PSBs) in this space witnessed a modest increase, from 23.5 per cent (1.6 crore outstanding cards) to 23.9 per cent (2.8 crore outstanding cards) over the same period. In contrast, the share of foreign banks saw a steep decline, from 9.3 per cent (50 lakh outstanding cards) to 3.8 per cent (44 lakh outstanding cards). Small Finance Banks had issued 14 lakh cards by December 2025, the report said.

Unlike credit cards, PSBs dominate the debit card space, although their market share has declined from 67.9 per cent (63.7 crore cards outstanding) in December 2021 to 63.1 per cent (65.2 crore cards outstanding) in December 2025, partly due to competition in payments posed by UPI.

During this period, however, private sector banks improved their share from 23.5 per cent (19.3 crore cards outstanding) to 25.1 per cent (26.0 crore cards outstanding).

“While credit cards are being increasingly used for online purchases and credit access, debit cards are mostly being used for cash withdrawals and basic transactions. Both instruments, however, face growing competition from digital alternatives,” said the report.

By mid-2025, India had over 111 crore cards in circulation, including around 11 crore credit cards, and more than 100 crore debit cards.

RTGS

However, the real, big money still flows through the trusted banking system’s heavyweight rails: RTGS handled just 0.1 per cent of transactions by volume but accounted for 68.6 per cent of the total transaction value.

Despite dominating everyday payments, UPI contributed only 9.5 per cent of the total transaction value.

The RBI had introduced the Real Time Gross Settlement (RTGS) system on March 26, 2004. Initially used for inter-bank transactions, it was expanded to settle customer transactions in April 2004. It currently operates round-the-clock (24×7). It is typically used for wholesale banking, corporate transfers, institutional settlements, and high-ticket transactions. The system requires a minimum transaction amount of Rs. 2 lakh, naturally resulting in low transaction count, but high transaction value.

The numbers highlight how India’s payment ecosystem has split mainly into two layers: UPI powering mass, low-value retail payments, and RTGS continuing to dominate high-value money movement.